The politicization

of ESG: What’s next?

The politicization

of ESG:

What’s next?

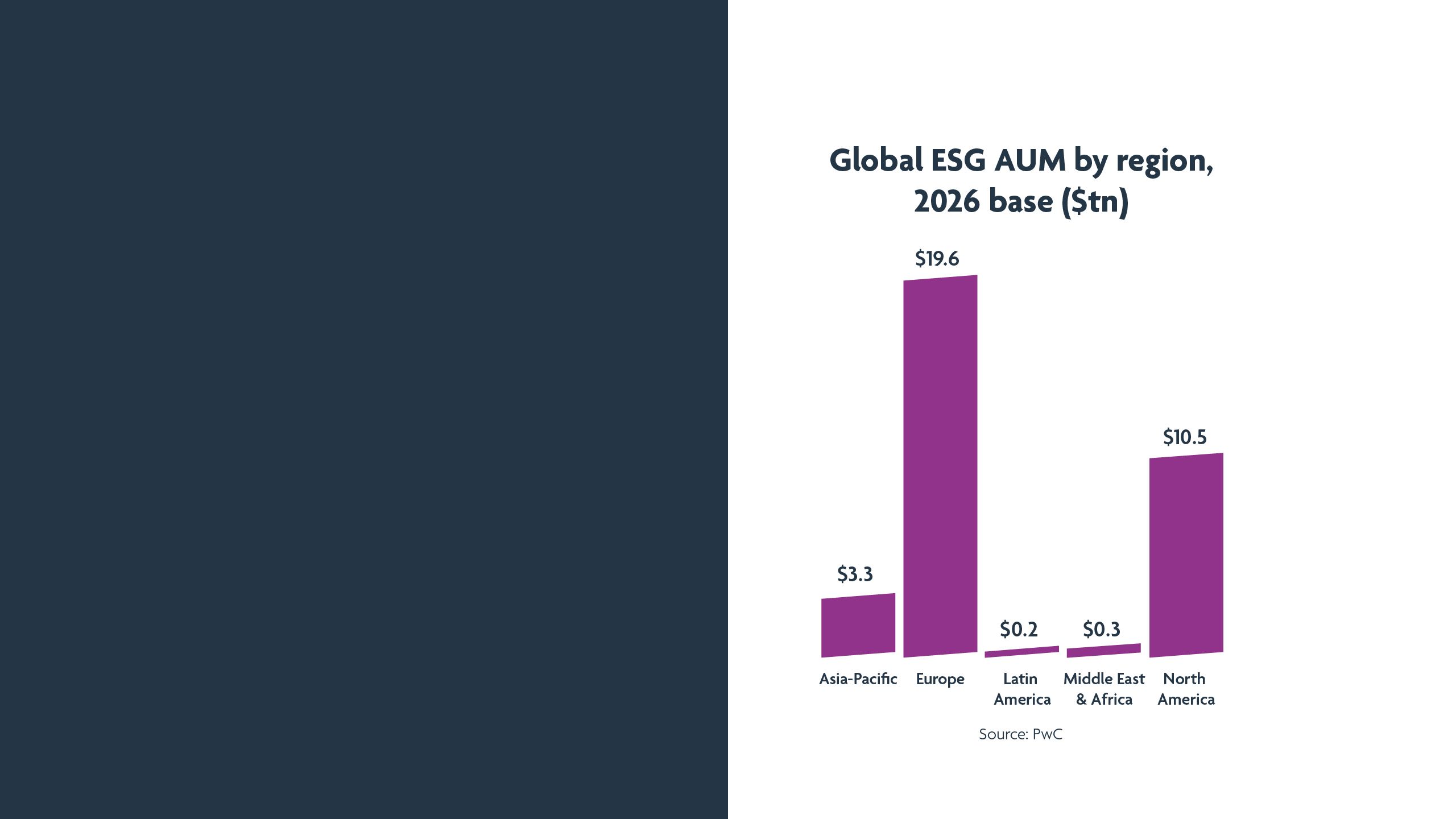

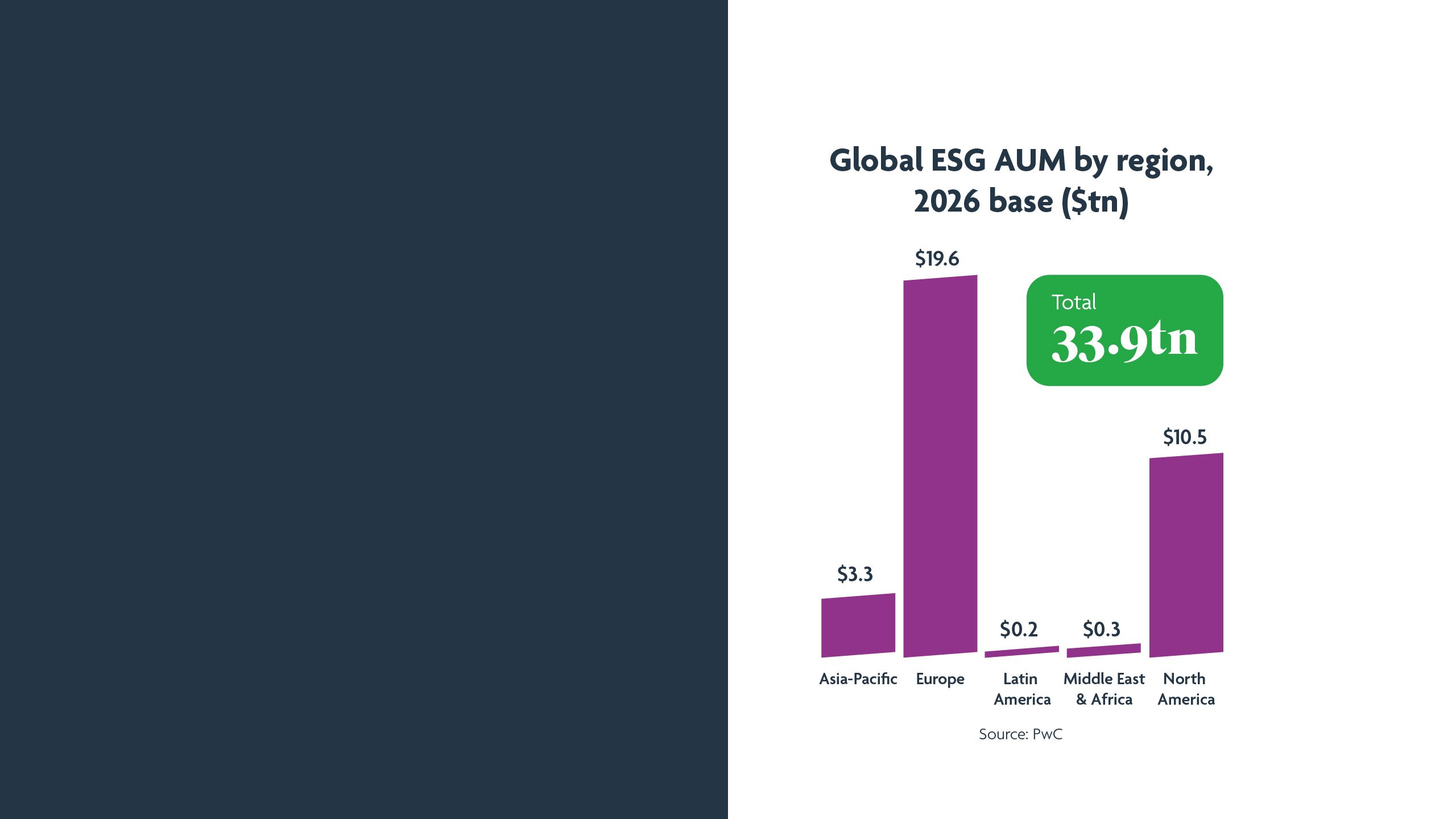

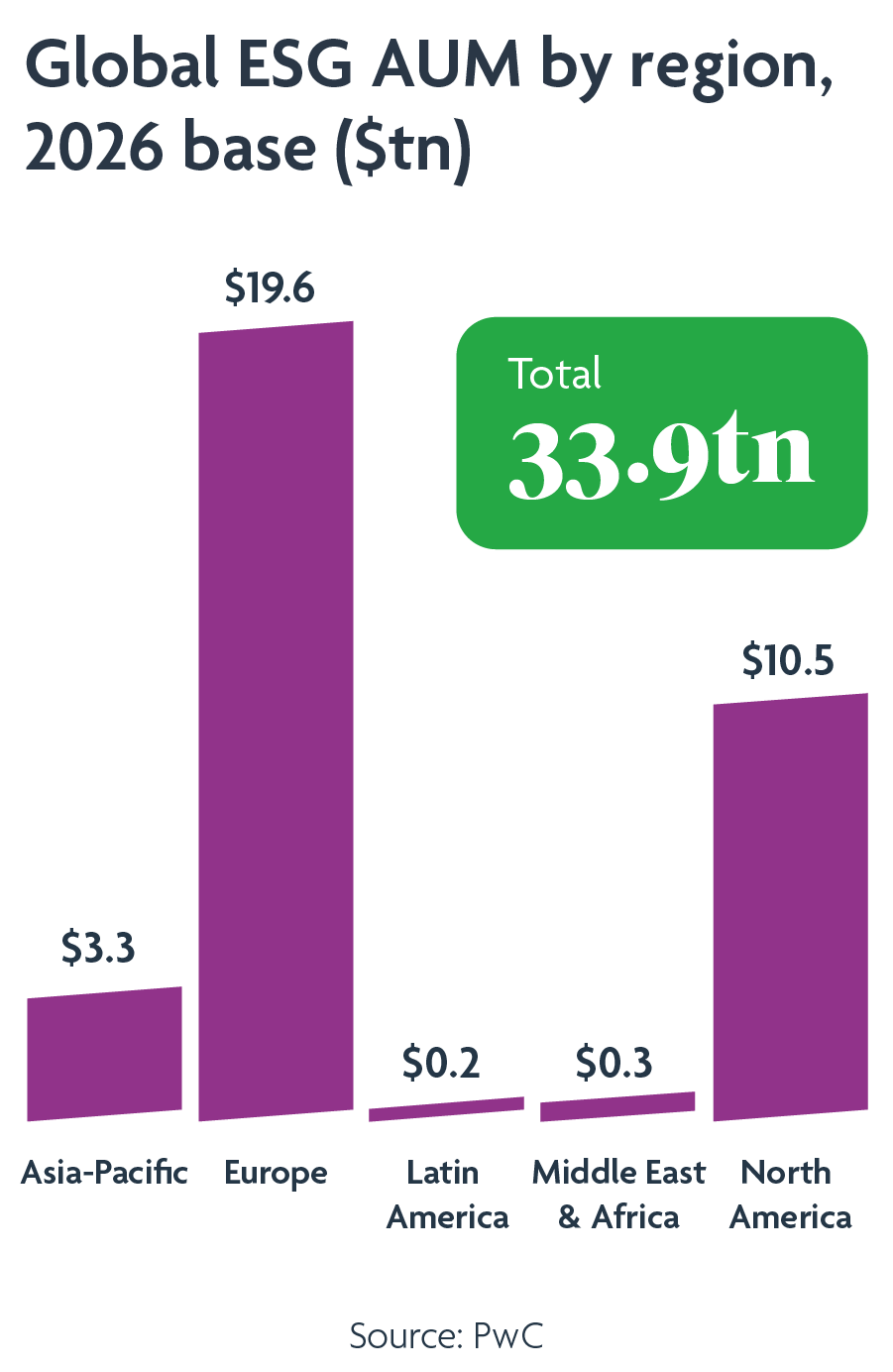

By all accounts, stakeholder demand for ESG-related products, disclosures and metrics across all sectors of the economy continued to grow over the course of 2022, and this is expected to continue unabated during 2023. A recent forecast by PwC projects that assets managers are expected to “increase their ESG-related assets under management to more than $34 trillion by 2026, from $18 trillion in 2021” as demand for ESG-related products – financial and otherwise – continues its recent growth trajectory. Nevertheless, there has been a growing and increasingly vocal anti-ESG sentiment that stakeholders must prepare to confront and address, particularly in the United States (U.S.).

By all accounts, stakeholder demand for ESG-related products, disclosures and metrics across all sectors of the economy continued to grow over the course of 2022, and this is expected to continue unabated during 2023. A recent forecast by PwC projects that assets managers are expected to “increase their ESG-related assets under management to more than $34 trillion by 2026, from $18 trillion in 2021” as demand for ESG-related products – financial and otherwise – continues its recent growth trajectory. Nevertheless, there has been a growing and increasingly vocal anti-ESG sentiment that stakeholders must prepare to confront and address, particularly in the United States (U.S.).

Indeed, skeptics have voiced doubts whether ESG actually facilitates long-term value creation or that adherence to ESG principles delivers results consistent with its promise. In some quarters, ESG-focused investing has been called a “scam” that has been “weaponized by social justice warriors”1. An opinion piece in The Wall Street Journal from October 2022 referred to a new $100 million energy index fund that will, in part, use “proxy measures to persuade companies to pursue…maximizing return to shareholders” in lieu of what is described as “politicized investment”2.

The politicization of ESG has been particularly evident in several states in the U.S. For instance, Florida and Texas, among others, submitted letters to major asset managers and pension administrators questioning whether ESG commitments are coming at the expense of shareholders, with several states pulling back billions of dollars that were invested with such asset managers. A handful of states have gone as far as prohibiting the consideration of ESG factors in connection with the investment of state pension and retirements funds. Criticism of ESG issues has not been limited to asset and investment managers – 21 Republican state attorneys general recently submitted letters to the two largest proxy voting advisory firms raising questions with respect to how those firms push ESG principles when making proxy-voting recommendations. Additionally, the most recent form of pushback has come from Republican members of the U.S. House of Representatives who have established an “ESG Working Group” to “combat the threat to our capital markets posed by those…pushing environmental, social, and governance (ESG) proposals”3.

Indeed, skeptics have voiced doubts whether ESG actually facilitates long-term value creation or that adherence to ESG principles delivers results consistent with its promise. In some quarters, ESG-focused investing has been called a “scam” that has been “weaponized by social justice warriors”1. An opinion piece in The Wall Street Journal from October 2022 referred to a new $100 million energy index fund that will, in part, use “proxy measures to persuade companies to pursue…maximizing return to shareholders” in lieu of what is described as “politicized investment”2.

The politicization of ESG has been particularly evident in several states in the U.S. For instance, Florida and Texas, among others, submitted letters to major asset managers and pension administrators questioning whether ESG commitments are coming at the expense of shareholders, with several states pulling back billions of dollars that were invested with such asset managers. A handful of states have gone as far as prohibiting the consideration of ESG factors in connection with the investment of state pension and retirements funds. Criticism of ESG issues has not been limited to asset and investment managers – 21 Republican state attorneys general recently submitted letters to the two largest proxy voting advisory firms raising questions with respect to how those firms push ESG principles when making proxy-voting recommendations. Additionally, the most recent form of pushback has come from Republican members of the U.S. House of Representatives who have established an “ESG Working Group” to “combat the threat to our capital markets posed by those…pushing environmental, social, and governance (ESG) proposals”3.

We expect the pushback against ESG to continue over the course of 2023 and that these efforts will ramp up significantly as we head into the 2024 presidential election season. That said, global demand for ESG-focused products and services may simply be too large to ignore or for anti-ESG proponents to gain material traction. In addition to PwC’s ESG-related growth projection noted above, jurisdictions outside of the U.S. have not seen any meaningful pushback relative to ESG issues. For example, and by comparison, in the EU and U.K., the politicization of ESG has been less prevalent, but as the Russia-Ukraine war continues, the energy crisis ceases to wane and political parties gear up for both local and national elections, it is expected that there will be similar issues brought to the forefront in a manner not dissimilar to the U.S. Relatedly, although asset managers have acknowledged that certain states have pulled back funds under investment, they are quick to note that divested funds are more than offset by capital inflows.

We expect the pushback against ESG to continue over the course of 2023 and that these efforts will ramp up significantly as we head into the 2024 presidential election season. That said, global demand for ESG-focused products and services may simply be too large to ignore or for anti-ESG proponents to gain material traction. In addition to PwC’s ESG-related growth projection noted above, jurisdictions outside of the U.S. have not seen any meaningful pushback relative to ESG issues. For example, and by comparison, in the EU and U.K., the politicization of ESG has been less prevalent, but as the Russia-Ukraine war continues, the energy crisis ceases to wane and political parties gear up for both local and national elections, it is expected that there will be similar issues brought to the forefront in a manner not dissimilar to the U.S. Relatedly, although asset managers have acknowledged that certain states have pulled back funds under investment, they are quick to note that divested funds are more than offset by capital inflows.

As stakeholders seek to navigate these complex issues, it is worth acknowledging that there are legitimate concerns related to ESG that need to be addressed.

As stakeholders seek to navigate these complex issues, it is worth acknowledging that there are legitimate concerns related to ESG that need to be addressed.

In addition, there are practical steps companies and other stakeholders can take to mitigate against legal and other risks in this space. Boards of directors and management teams, for instance, should review and evaluate ESG-related programs and policies regularly against broader long-term strategic growth strategies and initiatives to ensure alignment. Disclosure processes and procedures should be assessed to ensure that public disclosures and statements can be substantiated and hold up against greenwashing claims. Regulatory and rulemaking initiatives should be evaluated periodically with counsel and other professional advisors, particularly for companies that have operations in multiple or cross-border jurisdictions with potentially inconsistent approaches to these issues. Finally, all stakeholders will surely benefit from regular and open communications so as to ensure alignment of purpose and to avoid unnecessary conflict where possible.

In addition, there are practical steps companies and other stakeholders can take to mitigate against legal and other risks in this space. Boards of directors and management teams, for instance, should review and evaluate ESG-related programs and policies regularly against broader long-term strategic growth strategies and initiatives to ensure alignment. Disclosure processes and procedures should be assessed to ensure that public disclosures and statements can be substantiated and hold up against greenwashing claims. Regulatory and rulemaking initiatives should be evaluated periodically with counsel and other professional advisors, particularly for companies that have operations in multiple or cross-border jurisdictions with potentially inconsistent approaches to these issues. Finally, all stakeholders will surely benefit from regular and open communications so as to ensure alignment of purpose and to avoid unnecessary conflict where possible.

Authors

Kerry E. Berchem

Partner

Martine E. Cicconi

Partner

Amy Kennedy

Partner

Stacey H. Mitchell

Partner

shmitchell@akingump.com

Washington, D.C.

T+1 202.887.4338

v-card

Christopher A. Treanor

Counsel