The evolving

role of ESG in

shareholder activism

The evolving role of ESG

in shareholder activism

Shareholder activism continues to play a critical role in capital markets and we see no reason to think 2023 will play out any differently. Traditional activists are expected to continue pushing for issuers to implement changes that they believe will generate enhanced economic returns, such as modifications to a company’s capital or governance structures and changes in strategic and operational direction, capital expenditures and other items. The overall political and macroeconomic environments, coupled with investor fears regarding a potential recession and ongoing inflationary pressures are expected to result in activists continuing to aggressively push for companies to be responsive to their agendas. Additionally, companies across all sectors find themselves responding to demands for ESG-focused financial and consumer products and services, with such demands being made in a regulatory environment that is focused squarely on protecting stakeholders against greenwashing and other manipulative practices.

Within this context, activists are increasingly focusing on ESG considerations as they develop and promote their agendas, with some observing that attention to ESG issues can be linked with operational resilience, long-term competitiveness and enhanced financial returns. An analysis published by Broadridge indicated that ESG-related proposals increased by 25% in 20221, with the increase primarily attributable to proposals involving climate and social issues. These proposals can focus on both financial (e.g., measures aimed at enhancing long-term sustainable growth) and non-financial agendas (e.g., advocating for increased boardroom diversity, broader DEI and social justice initiatives) and do so using a growing variety of tactics and strategies2. ESG shareholder activism is sometimes justified by the financially driven thesis that more progressive companies will ultimately deliver greater shareholder returns as they move in alignment with consumer demands. Other shareholders may simply see it as the right thing to do. Whatever the rationale, ESG shareholder activism increasingly represents an external pressure from shareholders on issuers to adapt. Even investors that have purchased relatively small percentages in issuers have demonstrated their ability to corral sufficient support to impact the way in which significant businesses are run.

Shareholder activism continues to play a critical role in capital markets and we see no reason to think 2023 will play out any differently. Traditional activists are expected to continue pushing for issuers to implement changes that they believe will generate enhanced economic returns, such as modifications to a company’s capital or governance structures and changes in strategic and operational direction, capital expenditures and other items. The overall political and macroeconomic environments, coupled with investor fears regarding a potential recession and ongoing inflationary pressures are expected to result in activists continuing to aggressively push for companies to be responsive to their agendas. Additionally, companies across all sectors find themselves responding to demands for ESG-focused financial and consumer products and services, with such demands being made in a regulatory environment that is focused squarely on protecting stakeholders against greenwashing and other manipulative practices.

Within this context, activists are increasingly focusing on ESG considerations as they develop and promote their agendas, with some observing that attention to ESG issues can be linked with operational resilience, long-term competitiveness and enhanced financial returns. An analysis published by Broadridge indicated that ESG-related proposals increased by 25% in 20221, with the increase primarily attributable to proposals involving climate and social issues. These proposals can focus on both financial (e.g., measures aimed at enhancing long-term sustainable growth) and non-financial agendas (e.g., advocating for increased boardroom diversity, broader DEI and social justice initiatives) and do so using a growing variety of tactics and strategies2. ESG shareholder activism is sometimes justified by the financially driven thesis that more progressive companies will ultimately deliver greater shareholder returns as they move in alignment with consumer demands. Other shareholders may simply see it as the right thing to do. Whatever the rationale, ESG shareholder activism increasingly represents an external pressure from shareholders on issuers to adapt. Even investors that have purchased relatively small percentages in issuers have demonstrated their ability to corral sufficient support to impact the way in which significant businesses are run.

Traditionally, activist shareholders (e.g., institutional investors, hedge funds and other investors) have deployed a handful of tools to push their agendas. Typically, these tools have included pushing for greater shareholder engagement, sponsoring shareholder proposals, “vote no” campaigns and proxy contests. More aggressive activists may turn to threatening or actually engaging in litigation to pursue a particular goal. Obviously, a tactic that works for one activist may not be effective, or even an option, for another, depending on the facts and circumstances. Nevertheless, over the last few years, activists pushing ESG-focused agendas are increasingly leveraging these tools in both traditional and new ways in an effort to compel companies to pursue objectives that are consistent with ESG principles. To date, ESG-focused activists have focused primarily on the environmental and social aspects of ESG. That said, addressing governance issues (e.g., seeking changes to board composition and governance structures, protecting shareholder rights, or tying executive compensation to ESG-related metrics), is becoming a more significant tool.

Traditionally, activist shareholders (e.g., institutional investors, hedge funds and other investors) have deployed a handful of tools to push their agendas. Typically, these tools have included pushing for greater shareholder engagement, sponsoring shareholder proposals, “vote no” campaigns and proxy contests. More aggressive activists may turn to threatening or actually engaging in litigation to pursue a particular goal. Obviously, a tactic that works for one activist may not be effective, or even an option, for another, depending on the facts and circumstances. Nevertheless, over the last few years, activists pushing ESG-focused agendas are increasingly leveraging these tools in both traditional and new ways in an effort to compel companies to pursue objectives that are consistent with ESG principles. To date, ESG-focused activists have focused primarily on the environmental and social aspects of ESG. That said, addressing governance issues (e.g., seeking changes to board composition and governance structures, protecting shareholder rights, or tying executive compensation to ESG-related metrics), is becoming a more significant tool.

For example, in December 2020, the hedge fund Engine No. 1 invested $40 million in ExxonMobil Corporation, representing a stake of just 0.02%. The fund’s founder immediately published an open letter to the board of directors calling for radical strategic change in order to adapt to a low-carbon economy. Engine No. 1 argued that ExxonMobil had no strategy for navigating the carbon transition and that $170 billion of shareholder value had been destroyed by poor capital allocation. This letter garnered support from multiple institutional investors, who agreed with the premise that long term board members were not as sensitive as they should be to environmental issues and, ultimately, led to the appointment to the board of three activist-nominated directors with more experience in alternative fuels and energy. This example demonstrates that even with a small percentage shareholding, proactive investors can generate significant change where their campaign resonates with and receives support from major institutional investors that have an eye on their portfolio companies’ ESG strategies.

In the United Kingdom (U.K.), Bluebell Capital Partners, a London-based activist, began in February 2022 to push Glencore plc to demerge its coal mining business, on both financial and environmental grounds, but to maintain voting control via a dual-class share structure so Glencore can ensure mines are properly decommissioned once extraction ceases3. In April, Bluebell Capital then voted against approving Glencore’s 2021 Climate Progress Report4; with shareholder dissent of almost 24%, the approval of the 2021 Climate Progress Report was the least-supported resolution at Glencore’s 2022 annual general meeting5. While Glencore has not adopted Bluebell Capital Partners’ plans, it did commit in December 2022 to closing 12 coalmines by 2035 in order to meet emissions targets6. Nevertheless, this may not be enough to satisfy investors, with Legal & General and HSBC subsequently filing a resolution (to be voted on at the company’s annual general meeting in May 2023) requesting more detail on Glencore’s coal production plans7.

For example, in December 2020, the hedge fund Engine No. 1 invested $40 million in ExxonMobil Corporation, representing a stake of just 0.02%. The fund’s founder immediately published an open letter to the board of directors calling for radical strategic change in order to adapt to a low-carbon economy. Engine No. 1 argued that ExxonMobil had no strategy for navigating the carbon transition and that $170 billion of shareholder value had been destroyed by poor capital allocation. This letter garnered support from multiple institutional investors, who agreed with the premise that long term board members were not as sensitive as they should be to environmental issues and, ultimately, led to the appointment to the board of three activist-nominated directors with more experience in alternative fuels and energy. This example demonstrates that even with a small percentage shareholding, proactive investors can generate significant change where their campaign resonates with and receives support from major institutional investors that have an eye on their portfolio companies’ ESG strategies.

In the United Kingdom (U.K.), Bluebell Capital Partners, a London-based activist, began in February 2022 to push Glencore plc to demerge its coal mining business, on both financial and environmental grounds, but to maintain voting control via a dual-class share structure so Glencore can ensure mines are properly decommissioned once extraction ceases3. In April, Bluebell Capital then voted against approving Glencore’s 2021 Climate Progress Report4; with shareholder dissent of almost 24%, the approval of the 2021 Climate Progress Report was the least-supported resolution at Glencore’s 2022 annual general meeting5. While Glencore has not adopted Bluebell Capital Partners’ plans, it did commit in December 2022 to closing 12 coalmines by 2035 in order to meet emissions targets6. Nevertheless, this may not be enough to satisfy investors, with Legal & General and HSBC subsequently filing a resolution (to be voted on at the company’s annual general meeting in May 2023) requesting more detail on Glencore’s coal production plans7.

It is important to acknowledge that ESG activist investing is no longer an area where only smaller, ethically-driven investors are moving the needle. This has resulted in some significant backlash at the state and federal levels. Such backlash notwithstanding, asset managers continue to see significant capital inflows into, and demand for, ESG- or sustainability-linked products and such demand is not expected to recede for the foreseeable future.

Relatedly, proxy advisory firms, such as Institutional Shareholder Services Inc. and Glass Lewis, also are increasingly playing an important role in shareholder voting decisions as they publish more and more detailed and goal-oriented proxy voting guidelines. Reportedly, some investors have criticized asset managers and the proxy advisory firms for publishing guidelines that are overly prescriptive, while other investors may complain that such guidelines are not sufficiently aligned with particular ESG-related goals. In response, some asset managers have adopted pass-through voting programs so that investors can bypass voting guidelines they view as inadequate or lacking sufficient alignment with their broader goals8. This relatively new development may inject additional complexities into how companies manage shareholder votes in the future and will necessitate robust shareholder engagement programs so that companies understand which guidelines or procedures are guiding a particular shareholder vote or campaign.

It is important to acknowledge that ESG activist investing is no longer an area where only smaller, ethically-driven investors are moving the needle. This has resulted in some significant backlash at the state and federal levels. Such backlash notwithstanding, asset managers continue to see significant capital inflows into, and demand for, ESG- or sustainability-linked products and such demand is not expected to recede for the foreseeable future.

Relatedly, proxy advisory firms, such as Institutional Shareholder Services Inc. and Glass Lewis, also are increasingly playing an important role in shareholder voting decisions as they publish more and more detailed and goal-oriented proxy voting guidelines. Reportedly, some investors have criticized asset managers and the proxy advisory firms for publishing guidelines that are overly prescriptive, while other investors may complain that such guidelines are not sufficiently aligned with particular ESG-related goals. In response, some asset managers have adopted pass-through voting programs so that investors can bypass voting guidelines they view as inadequate or lacking sufficient alignment with their broader goals8. This relatively new development may inject additional complexities into how companies manage shareholder votes in the future and will necessitate robust shareholder engagement programs so that companies understand which guidelines or procedures are guiding a particular shareholder vote or campaign.

At the more aggressive end of the spectrum, some more combative activist groups have resorted to aggressive litigation to pursue their goals, particularly in relation to environmental matters. For instance, the successful claim by almost 2,000 Zambian villagers against Vedanta Resources plc9 based on environmental pollution has paved the way for group litigation10 against parent companies whose subsidiaries are alleged to be causing environmental damage. Such class actions are often funded and driven by specialist litigation funders who also may be working with activist investors. Similarly, activist ClientEarth has taken French food producer Danone to court in Paris11 based on its failure to sufficiently reduce its plastic footprint in packaging.

At the more aggressive end of the spectrum, some more combative activist groups have resorted to aggressive litigation to pursue their goals, particularly in relation to environmental matters. For instance, the successful claim by almost 2,000 Zambian villagers against Vedanta Resources plc9 based on environmental pollution has paved the way for group litigation10 against parent companies whose subsidiaries are alleged to be causing environmental damage. Such class actions are often funded and driven by specialist litigation funders who also may be working with activist investors. Similarly, activist ClientEarth has taken French food producer Danone to court in Paris11 based on its failure to sufficiently reduce its plastic footprint in packaging.

In a development arising primarily outside of the U.S., ESG litigation also can come from within a company itself. In May 2021, the Hague District Court ordered Shell to reduce emissions by 45% from 2019 levels by 2030 (currently under appeal by Shell12), in line with the Paris Agreement. Subsequently, in March 2022, ClientEarth took a derivative action on behalf of Shell plc against Shell’s board of directors13, alleging that the board’s failure to adopt and implement an adequate climate strategy to comply with this previous judgement was in breach of the directors’ duties under section 172 of the U.K. Companies Act 2006 to promote the success of the company. A pre-action letter of claim was sent by ClientEarth to the board in March 2022. There have been no public updates since then.

In a development arising primarily outside of the U.S., ESG litigation also can come from within a company itself. In May 2021, the Hague District Court ordered Shell to reduce emissions by 45% from 2019 levels by 2030 (currently under appeal by Shell12), in line with the Paris Agreement. Subsequently, in March 2022, ClientEarth took a derivative action on behalf of Shell plc against Shell’s board of directors13, alleging that the board’s failure to adopt and implement an adequate climate strategy to comply with this previous judgement was in breach of the directors’ duties under section 172 of the U.K. Companies Act 2006 to promote the success of the company. A pre-action letter of claim was sent by ClientEarth to the board in March 2022. There have been no public updates since then.

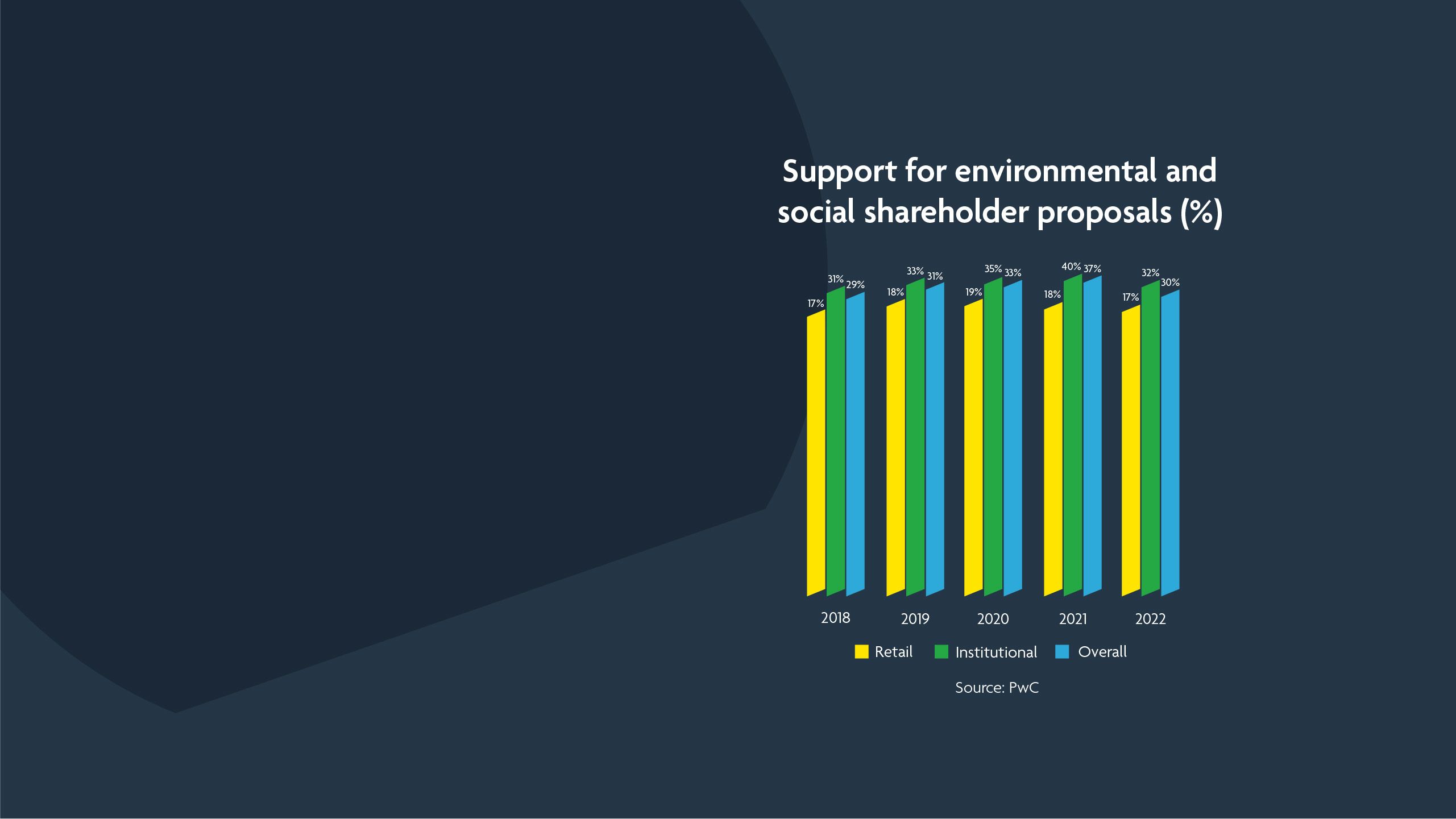

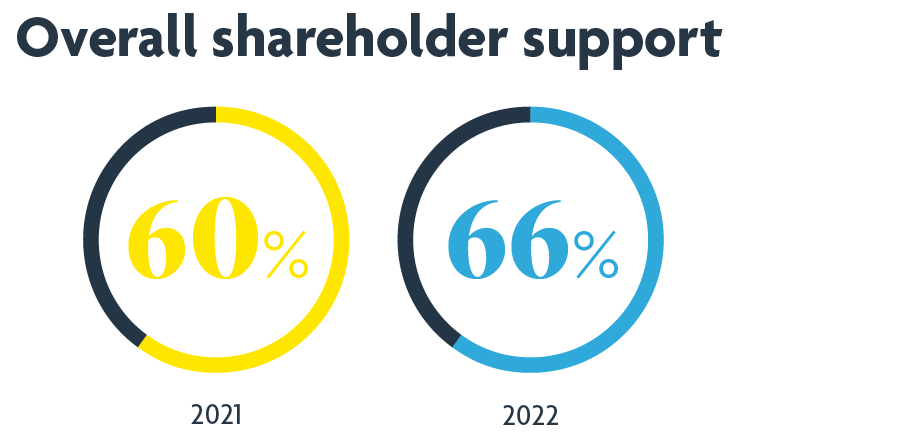

Despite the increasing influence of ESG factors in the activist space, there has been a recent trend from certain institutional investors not to support shareholder-proposed ESG resolutions. Non-profit campaigner ShareAction, which tracks the ESG voting performance of institutional investors, found that asset managers (including The Vanguard Group, Inc. and State Street Corporation), supported fewer ESG shareholder proposals in 2022 than in 2021, despite overall shareholder support growing from 60% to 66% during the same period.

One reason for this may be boards reacting in a proactive, defensive manner to the waves of ESG activist activity seen in recent years by adapting their strategies to take into account some of the activists’ usual concerns. However, one anonymous asset manager has expressed concerns that these proposals are becoming increasingly prescriptive, ignoring financial performance and, in some cases, targeting issues on which the company in question has already made notable progress. Meanwhile, political opposition to ESG-based investment in certain U.S. states has served to discourage institutions from supporting shareholder proposals, with the same anonymous asset manager suggesting that it would have lost its license to operate in the U.S. had it supported all ESG resolutions14.

Nevertheless, for investors with an appetite to drive change, ESG-focused activist opportunities still abound. In the first half of 2022, activist campaigns at S&P 500 companies increased 42.5% percent over the same period in 202115, and in Europe, they increased by 67%16. There are also various predictions for more opportunities for activist investors through ESG-focused campaigns in 202317. Prudent investors will no doubt bear these issues in mind when planning investment strategies for the year ahead.

One reason for this may be boards reacting in a proactive, defensive manner to the waves of ESG activist activity seen in recent years by adapting their strategies to take into account some of the activists’ usual concerns. However, one anonymous asset manager has expressed concerns that these proposals are becoming increasingly prescriptive, ignoring financial performance and, in some cases, targeting issues on which the company in question has already made notable progress. Meanwhile, political opposition to ESG-based investment in certain U.S. states has served to discourage institutions from supporting shareholder proposals, with the same anonymous asset manager suggesting that it would have lost its license to operate in the U.S. had it supported all ESG resolutions14.

Nevertheless, for investors with an appetite to drive change, ESG-focused activist opportunities still abound. In the first half of 2022, activist campaigns at S&P 500 companies increased 42.5% percent over the same period in 202115, and in Europe, they increased by 67%16. There are also various predictions for more opportunities for activist investors through ESG-focused campaigns in 202317. Prudent investors will no doubt bear these issues in mind when planning investment strategies for the year ahead.

Authors

Kerry E. Berchem

Partner

Harry Keegan

Partner

Jason Koenig

Partner

jkoenig@akingump.com

New York

T+1 212.872.8182

F+1 212.872.1002

v-card

Vance Chapman

Partner

Charles Edward Smith

Consultant