“I thought you said

this was ESG-friendly?!” –

Risks associated with greenwashing/green-hushing

“I thought you said this was ESG-friendly?!”:

Risks associated with greenwashing/green-hushing

As ESG factors are integrated more and more frequently across industries and products, so too are risks associated with “greenwashing” and “green-hushing.” Greenwashing is the act of providing stakeholders (e.g., investors and consumers) with misleading or false information about whether a product was produced using sustainable practices or is itself sustainable. Greenwashing also can be deployed by companies in order to mask how certain business operations or practices may, in fact, adversely affect the environment, for instance. The term can apply equally to financial products and/or services (e.g., where the product is marketed as being environmentally friendly or its returns are linked to the achievement of certain sustainability metrics).

Relatedly, green-hushing occurs when a company opts to stay quiet or less vocal regarding its environmental, climate or other ESG goals and strategies. According to the Corporate Governance Institute, there are two primary reasons companies engage in green-hushing: first, they do not want to risk being exposed to negative publicity if they fail to achieve a publicly disclosed goal or target; and second, they do not want to risk greenwashing claims if it turns out their results are less than promised or suggested.

Over the course of 2022, there was a marked uptick in the attention stakeholders are paying to these issues. In response, regulators across the globe and all industries undertook extensive rulemaking initiatives that were, ostensibly, designed to protect investors, consumers and other relevant parties against greenwashing. In the United States (U.S.), these efforts were spearheaded primarily by the U.S. Securities and Exchange Commission (SEC) and other federal regulatory agencies. Indeed, the SEC proposed new disclosure requirements that are specifically intended to address greenwashing, including proposals related to climate risk, cybersecurity, investment managers and ESG more broadly1.

Relatedly, green-hushing occurs when a company opts to stay quiet or less vocal regarding its environmental, climate or other ESG goals and strategies. According to the Corporate Governance Institute, there are two primary reasons companies engage in green-hushing: first, they do not want to risk being exposed to negative publicity if they fail to achieve a publicly disclosed goal or target; and second, they do not want to risk greenwashing claims if it turns out their results are less than promised or suggested.

Over the course of 2022, there was a marked uptick in the attention stakeholders are paying to these issues. In response, regulators across the globe and all industries undertook extensive rulemaking initiatives that were, ostensibly, designed to protect investors, consumers and other relevant parties against greenwashing. In the United States (U.S.), these efforts were spearheaded primarily by the U.S. Securities and Exchange Commission (SEC) and other federal regulatory agencies. Indeed, the SEC proposed new disclosure requirements that are specifically intended to address greenwashing, including proposals related to climate risk, cybersecurity, investment managers and ESG more broadly1.

Consistent with past practice, regulators in the European Union (EU) and U.K. have, generally speaking, outpaced their U.S. counterparts. For instance, during 2023, lawmakers in Europe are reportedly preparing to put forward a series of proposals that are intended to address greenwashing across various products. In fact, just last month, the European Commission published the “Green Claims Directive,” which is intended, among other things, to set forth the first set of comprehensive rules to ensure that businesses do not engage in greenwashing when it comes to claims involving sustainability or ESG-related impacts. If adopted, these initiatives would require companies to ensure that any climate-related or environmental assertions companies make are backed by science. Similarly, in the U.K., regulators have proposed a series of rules that would, if adopted, attempt to prevent consumers from being misled. These proposals would require disclosures so that consumers can more clearly understand a product’s sustainability features and limit the usage of terms such as “ESG” and “green.”

Regulators in Asia have likewise turned their attention to greenwashing, with regulators in Japan, Hong Kong and Singapore looking at various measures that can be used to combat greenwashing and protect consumers and investors. These efforts have included the adoption or development of green taxonomies by at least 13 countries, as well as the publication of a sustainable finance taxonomy by the Association of Southeast Asian Nations2. Similarly, progress has been made on disclosure requirements, including a new requirement proposed by the Monetary Authority of Singapore to require that asset managers make climate-related disclosures that align with standards promulgated by the International Sustainability Standards Board (ISSB)3.

Consistent with past practice, regulators in the European Union (EU) and U.K. have, generally speaking, outpaced their U.S. counterparts. For instance, during 2023, lawmakers in Europe are reportedly preparing to put forward a series of proposals that are intended to address greenwashing across various products. In fact, just last month, the European Commission published the “Green Claims Directive,” which is intended, among other things, to set forth the first set of comprehensive rules to ensure that businesses do not engage in greenwashing when it comes to claims involving sustainability or ESG-related impacts. If adopted, these initiatives would require companies to ensure that any climate-related or environmental assertions companies make are backed by science. Similarly, in the U.K., regulators have proposed a series of rules that would, if adopted, attempt to prevent consumers from being misled. These proposals would require disclosures so that consumers can more clearly understand a product’s sustainability features and limit the usage of terms such as “ESG” and “green.”

Regulators in Asia have likewise turned their attention to greenwashing, with regulators in Japan, Hong Kong and Singapore looking at various measures that can be used to combat greenwashing and protect consumers and investors. These efforts have included the adoption or development of green taxonomies by at least 13 countries, as well as the publication of a sustainable finance taxonomy by the Association of Southeast Asian Nations2. Similarly, progress has been made on disclosure requirements, including a new requirement proposed by the Monetary Authority of Singapore to require that asset managers make climate-related disclosures that align with standards promulgated by the International Sustainability Standards Board (ISSB)3.

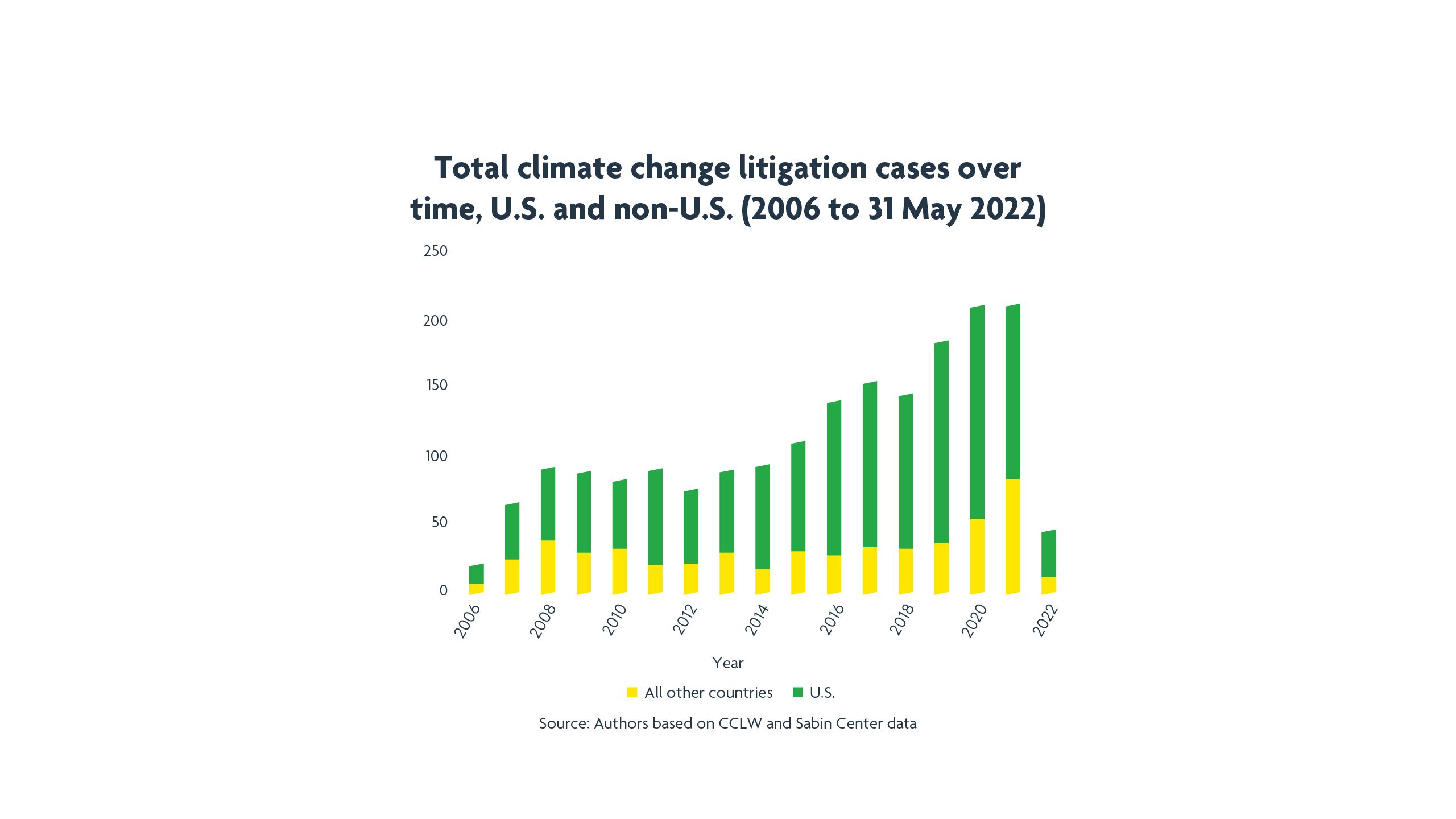

Litigation and regulatory actions involving greenwashing claims increased during 2022 and are apt to continue to rise during 2023. Claimants are using a broad set of legal theories to advance these efforts including claims alleging violations of consumer protection laws (e.g., misrepresentation on product labels); claims challenging ESG-related statements, reports or other marketing materials (e.g., sustainability claims on company websites or on product labels); deceptive or unfair business practices claims (e.g., violations of the “Green Guides” issued by the Federal Trade Commission); and securities fraud claims (e.g., inadequate or misleading disclosures). Increasingly, claimants are alleging greenwashing claims across a company’s supply chain, with litigants focused on human rights violations and trafficking and whether companies are adequately undertaking due diligence with respect to whether their suppliers are complying with applicable law and best practices in the procurement process.

As is usually the case, there are some practical steps companies can take in order to mitigate against greenwashing risks in their business operations.

Companies should evaluate existing disclosures relating to ESG and sustainability and undertake due diligence to check whether such disclosures can be substantiated. When looking at the statements themselves, consider whether a more aspirational, less concrete statement may be advisable relative to referencing concrete statements or metrics. Relatedly, companies should review existing disclosure policies and practices to identify any gaps or areas for improvement, particularly if a company is making voluntary disclosures that are aligned with a third-party disclosure framework (e.g., Task Force on Climate-related Financial Disclosures (TCFD)). Also, consider whether any disclosures should be accompanied with appropriate disclaimers or caveats. A board of directors should carefully consider how to discharge its duty of oversight relative to ESG and related issues (e.g., vest an existing board committee with oversight responsibilities or create a stand-alone committee for that purpose). Finally, businesses should regularly review regulatory guidance and developments and, as always, consult with relevant professionals and attorneys to remain “on-side” relative to these issues.

Litigation and regulatory actions involving greenwashing claims increased during 2022 and are apt to continue to rise during 2023. Claimants are using a broad set of legal theories to advance these efforts including claims alleging violations of consumer protection laws (e.g., misrepresentation on product labels); claims challenging ESG-related statements, reports or other marketing materials (e.g., sustainability claims on company websites or on product labels); deceptive or unfair business practices claims (e.g., violations of the “Green Guides” issued by the Federal Trade Commission); and securities fraud claims (e.g., inadequate or misleading disclosures). Increasingly, claimants are alleging greenwashing claims across a company’s supply chain, with litigants focused on human rights violations and trafficking and whether companies are adequately undertaking due diligence with respect to whether their suppliers are complying with applicable law and best practices in the procurement process.

As is usually the case, there are some practical steps companies can take in order to mitigate against greenwashing risks in their business operations.

Companies should evaluate existing disclosures relating to ESG and sustainability and undertake due diligence to check whether such disclosures can be substantiated. When looking at the statements themselves, consider whether a more aspirational, less concrete statement may be advisable relative to referencing concrete statements or metrics. Relatedly, companies should review existing disclosure policies and practices to identify any gaps or areas for improvement, particularly if a company is making voluntary disclosures that are aligned with a third-party disclosure framework (e.g., Task Force on Climate-related Financial Disclosures (TCFD)). Also, consider whether any disclosures should be accompanied with appropriate disclaimers or caveats. A board of directors should carefully consider how to discharge its duty of oversight relative to ESG and related issues (e.g., vest an existing board committee with oversight responsibilities or create a stand-alone committee for that purpose). Finally, businesses should regularly review regulatory guidance and developments and, as always, consult with relevant professionals and attorneys to remain “on-side” relative to these issues.

Authors

Stacey H. Mitchell

Partner

shmitchell@akingump.com

Washington, D.C.

T+1 202.887.4338

v-card

Stephanie Lindemuth

Partner